Biologic drugs represent advances in medical research and treatment but are a major driver of drug spending in the United States. Spending on biologics increased by 50% between 2014 and 2018 in the U.S. even though just 2% of Americans used them. Biosimilars, clinically equivalent, lower-cost versions of original biologic drugs, analogous to generic versions of brand name “small molecule” drugs, could reduce this spending. Biosimilars are much more common in Europe than in the U.S. The first biosimilar in Europe was approved in 2006, and their use has increased since, leading to lower spending. In the U.S., biosimilar approvals have been slower. The first biosimilar in the U.S. was approved and launched in late 2015. As of December 2022, the FDA has approved 40 of them. In 2023, as many as 10 biosimilars are poised to become available for the blockbuster drug adalimumab (Humira), potentially saving the U.S. health care system billions of dollars.

In this brief, we examined the use, spending, and price of biosimilars among people with employer-sponsored insurance (ESI) between 2019 and 2021 using data from the Health Care Cost Institute. We focused on seven drug product classes that had approved and market-launched biosimilars in this period. These drugs are physician-administered injections and infusions and, therefore, are administered under the supervision of a health care professional. The drugs were:

- Trastuzumab, rituximab, and bevacizumab, which are used to treat specific kinds of cancer.

- Pegfilgrastim and filgrastim, which are used to reduce the risk of infection in patients who are undergoing chemotherapy or radiation.

- Infliximab, which is used to treat rheumatoid arthritis and other autoimmune diseases.

- Epoetin, which is used to treat anemia in people with kidney failure, as supportive treatment of anemia caused by chemotherapy, and to decrease the chance of blood loss during certain surgeries.

Total spending on these seven drug product classes, weighted to be representative of the national ESI population, was close to $31 billion over the 2019-2021 period (spending by drug product class and stratified by biologic and biosimilar are in the downloadable data accompanying this brief).

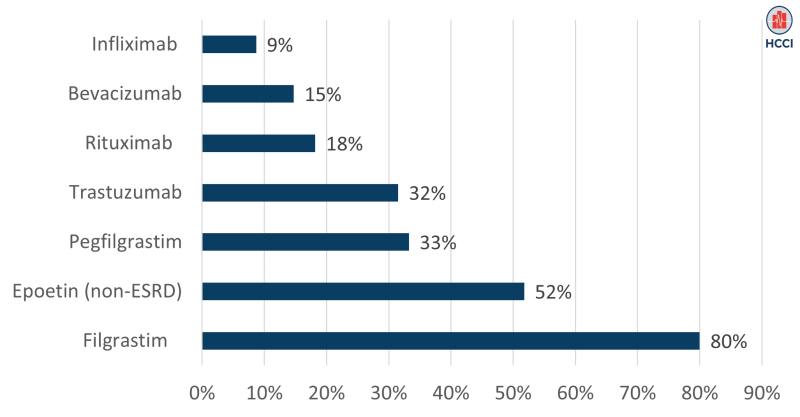

In Five of Seven Drug Classes, Biosimilars Accounted for One-Third or Less of ESI Use

In most of the drug product classes we studied, biosimilars made up one-third or less of all drug administrations (i.e., the majority of use was of the original biologic product, sometimes called the reference or originator biologic). As shown in Figure 1, the biosimilar infliximab was only 9% of use in its drug class (reference biologic: Remicade). Similarly, biosimilars made up under 20% of use of bevacizumab (reference biologic: Avastin) and rituximab (reference biologic: Rituxan), and about one-third of use of trastuzumab (reference biologic: Herceptin) and pegfilgrastim (reference biologic: Neulasta).

In contrast, biosimilars made up just over half of use of epoetin (reference biologics: Epogen and Procrit, looking only at use of epoetin among non-End Stage Renal Disease patients) and 80% of use of short-acting filgrastim products. Among short-acting filgrastim products, the reference biologic Neupogen made up only 20% of use in that class in 2021. The high biosimilar share in this class may reflect the fact that Neupogen was the first reference biologic to face biosimilar competition.

Figure 1: Biosimilar Use as a Share of All Administered Drug Use by Drug Class

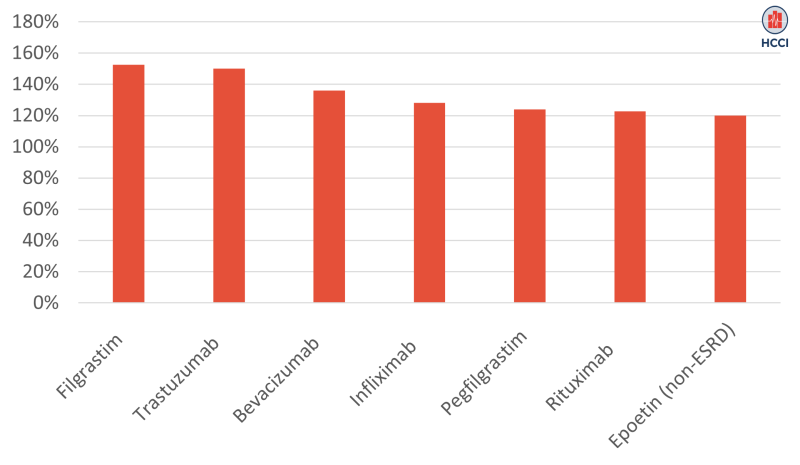

Biologic Drug Prices were 20%-50% Higher than Prices of Associated Biosimilars

As shown above, use of the reference biologic remains high in many drug classes even when biosimilars are available. Continued high use of biologics is likely to drive up spending due to price differences between biologics and biosimilars. We compared unit prices for reference biologics and their biosimilar equivalents in the HCCI data. The unit price allows us to compare prices independent of differences in dosage or clinical indication.

For all seven drug product classes we examined, the biologic price was at least 20% higher than the prices of associated biosimilars, as shown in Figure 2. The biggest price differences were for filgrastim and trastuzumab, where the biologic prices were about 50% higher than their biosimilar versions. The biologic unit price was 36% higher than the biosimilar for bevacizumab, and between 20% and 28% higher for the other four drug product classes.

Figure 2: Unit Price of Biologic as a Percentage of Biosimilar Price by Drug Class

Reference Biologic Use and Prices Remain High in ESI

Reference biologics make up the majority of all use in five of the seven drug product classes we examined, despite having meaningfully higher prices than available biosimilars. For biosimilars to fulfill projections of billions of dollars in savings in the health care system, more aggressive policies would need to induce greater biosimilar use, including placement on health plans’ preferred drug lists, shifting of provider supply to biosimilar options, or direct outreach to educate patients on clinical equivalence to alleviate concerns or hesitancy.

Previous HCCI research found that biosimilar savings in the ESI population have not kept pace with biosimilar savings in Medicare. This suggests that market entry of biosimilars have yet to generate drug price competition in the ESI population. Savings from biosimilars represent real financial opportunities for people with ESI, particularly for people who require these drugs to manage their health. This analysis suggests that there are opportunities for stakeholders to bring down drug spending by promoting adoption of biosimilars and facilitating greater price competition among existing reference biologic drugs.

Methods

We restricted our analysis to adjudicated outpatient facility and professional claims with an employer-sponsored insurer health plan as the primary payer and allowed amounts greater than $1 between 2019 and 2021. We identified biosimilar and reference biologic drugs of interest using Healthcare Common Procedure Coding System (HCPCS). Please refer to Table 1 below for HCPCS codes of interest found in HCCI data. We limited our analysis to drug products where there was at least one biosimilar market launched between 2019 and 2021. We removed Epoetin with ESRD indication from our analysis due to incomplete data among ESRD enrollees.

| Drug Product | Reference Biologic HCPCS | Biosimilar HCPCS |

| Bevacizumab | J9035 | Q5107, Q5118 |

| Epoetin (Non-ESRD) | J0885 | Q5106 |

| Filgrastim | J1442 | Q5101, Q5110 |

| Infliximab | J1745 | Q5102, Q5103, Q5104, Q5121 |

| Pegfilgrastim | J2505 | Q5108, Q5111, Q5120 |

| Rituximab | J9310, J9312 | Q5115, Q5119 |

| Trastuzumab | J9355 | Q5112, Q5113, Q5114, Q5116, Q5117 |