Biologic drugs include a range of life-saving medications to treat cancer, diabetes, rheumatoid arthritis, retinal diseases, and many other conditions. Unlike “small molecule” drugs (e.g., statins), which can generally be taken at home, biologics are typically infusions or injections which require administration by a physician or other clinician in a hospital or physician’s office. While just 2% of Americans use a biologic drug, the cost of these drugs to patients and insurers has drawn increasing attention from policymakers. Biologics often come with a hefty price tag; for example, the most commonly used biologic drug, HumiraTM, can have out-of-pocket costs that run up to $9,065 per month without insurance.

In the small molecule market, generic versions of brand name drugs have substantially lowered brand name prices. For biologics, the generic analog (i.e., clinically equivalent, lower-cost version) is known as a biosimilar. Because increases in biologic prices have consistently accounted for the majority of US annual drug spending growth, policymakers and researchers often cite the potential of biosimilars to generate savings over the next 5-10 years.

Recent research has shown that, when biosimilars become available, increased competition can lower the original biologic’s “average sales price” (ASP) set by the drug manufacturer. While Medicare payment for biologics and biosimilars is directly tied to the ASP, it is not clear whether decreases in ASP translate to a reduction in the prices that people who get their insurance through an employer, their employers, and insurers pay for these drugs.

In this brief, we used HCCI’s commercial claims dataset to assess the impact of biosimilar entry on savings among people with ESI compared to Medicare in the context of one biologic/biosimilar pair. We looked at the case of NeupogenTM (biologic), an injectable drug typically used to help cancer patients regain immunity following a course of chemotherapy, and its biosimiliar equivalent, ZarxioTM (filgrastim-sndz), the first biosimilar to receive FDA approval in 2015.

Between 2015 and 2020, we found that the relative prices of these two products in ESI did not change substantially. ZarxioTM remained about 20% lower in price than NeupogenTM over the study period in the ESI sample. In contrast, in Medicare over the same period, the unit price of ZarxioTM dropped to almost half the unit price of NeupogenTM. The absence of a declining price of ZarxioTM in ESI means that the savings associated with the biosimilar entry among ESI enrollees was much more limited than among Medicare enrollees.

This finding implies that, without additional regulatory pressure on prices, there may be limits to the impact of biosimilar entry on spending on administered drugs in ESI. Further, our results suggest that relying on traditional drug acquisition pricing data, such as ASP or drug distribution sales, to monitor overall drug prices trends might mask actual ESI drug prices because they do not capture actual negotiated prices. Instead, using administrative claims from commercial insurers allows policymakers and stakeholders to observe the actual paid amounts of drug administrations. In turn, using more representative data of what patients and insurers actually pay for these drugs will improve our understanding of patient access to these drugs.

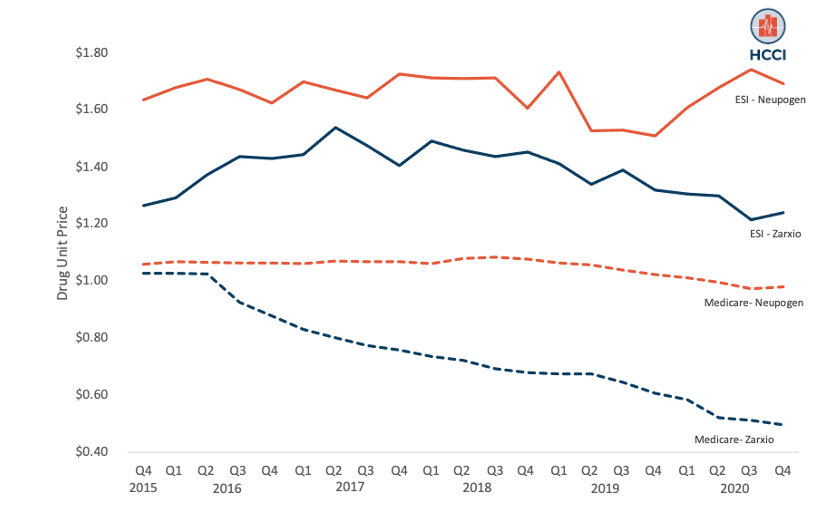

ESI Prices for the Biologic and Biosimilar were Higher than Medicare Prices

Our measures of unit prices for ZarxioTM and NeupogenTM differed between fee-for-service Medicare and ESI. In Medicare, the unit price for these two products is the ASP, which is assigned individually for each product for each quarter. We obtained ASP prices between Q4 2015 and Q4 2020 from the Centers for Medicare and Medicaid Services. To generate a comparable price in ESI, we calculated the quarterly unit price for ZarxioTM and NeupogenTM in HCCI’s commercial claims dataset between Q4 2015 and Q4 2020 as the total allowed amount (for each product in each quarter) over the total billed units of the product in the same quarter.

Throughout our 2015-2020 study period, the ESI unit reimbursement rate for NeupogenTM ($1.66) was 68% higher than the Medicare (ASP) unit reimbursement rate ($0.99) on average. We found an even sharper difference in the unit reimbursement rate for ZarxioTM between ESI and Medicare. The ESI price was 97% higher on average than the Medicare price ($1.38 compared to $0.70). Figure 1 shows the trend in unit prices for both ZarxioTM and NeupogenTM in Medicare and ESI. Prices for both products were consistently higher in ESI than in Medicare over the study period.

Figure 1: Unit Prices of ZarxioTM and NeupogenTM in ESI and Medicare

The Price for ZarxioTM Decreased in Medicare but Remained Flat in ESI

As shown in Figure 1, Medicare prices for both products declined in Medicare over the study period. Since its approval in 2015, the unit price of ZarxioTM in Medicare decreased steadily from $0.97 to $0.47 (decrease of 52%). Over the same period, NeupogenTM‘s Medicare prices decreased by 7.4% ($1.00 in Q4-2015 to $0.93 in Q4-2020). In contrast, prices for both products remained relatively flat in ESI over the study period. The price of ZarxioTM in ESI decreased just 1.8% from $1.26 in Q4-2015 to $1.24 in Q4-2020; NeupogenTM prices in ESI also remained constant during the study period ($1.64 in Q4-2015 to $1.69 in Q4-2020).

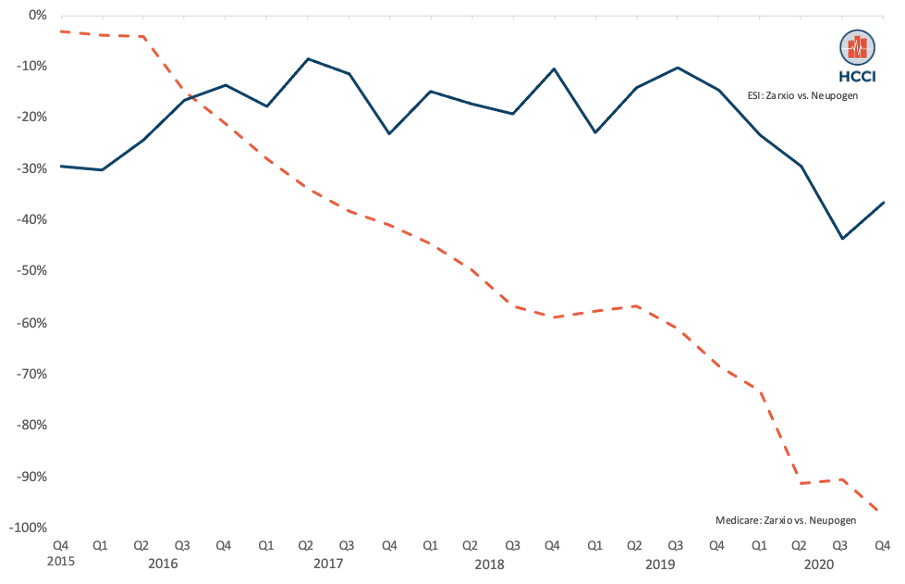

Savings Associated with ZarxioTM in ESI were Much Smaller than in Medicare

As seen in Figure 1, ESI unit prices for ZarxioTM and NeupogenTM remained relatively flat during the study period. In contrast, the Medicare unit price for ZarxioTM decreased considerably while the unit price for NeupogenTM decreasingly modestly, leading to higher savings from ZarxioTM‘s entry. To examine the savings associated with the introduction of ZarxioTM, we calculated the percentage difference between NeupogenTM and ZarxioTM unit prices in each quarter, i.e., the “discount” associated with ZarxioTM compared to NeupogenTM.

As shown in Figure 2, the Medicare unit prices of ZarxioTM and NeupogenTM were nearly the same in late 2015 and early 2016, but by 2020 the prices had diverged. By the end of 2020, the discount associated with ZarxioTM had reached almost 98% ($0.93 for NeupogenTM and $0.47 for ZarxioTM). In contrast, the discount associated with ZarxioTM remained consistently at 20% during this period among ESI ($1.69 for NeupogenTM and $1.24 for ZarxioTM). This was a substantially smaller discount than we observed in Medicare over the same period.

Figure 2: Relative Price (“Discount”) Associated with ZarxioTM Relative to NeupogenTM in ESI Compared to Medicare

Findings Point to Need to Monitor ESI-Specific Prices and Savings

Existing HCCI work has shown that prices paid by ESI enrollees and insurers are significantly higher than Medicare for medical services; in this blog, we observe similar patterns for administered drugs in the case of Neupogen and Zarxio. Given these price differences, the entry of biosimilars into the administered drugs market has the potential to lower drug prices in ESI dramatically. Using HCCI’s commercial claims data, however, we found that, in the case of ZarxioTM‘s entry, savings are far more modest in ESI than in Medicare.

Many policy projections of savings attributed to biosimilars rely on price metrics from Medicare (e.g., ASP or distribution drug sales data). Without full information on the impact of biosimilars among people with ESI, policymakers may be overestimating the savings attributed to biosimilars. Moreover, public and private decisionmakers should consider additional ESI-focused policies to achieve the savings promised by estimates based on Medicare data.

Understanding the impact of biosimilars in the ESI market will become increasingly important in 2023. While over 55 biosimilars have been approved for use and are offered to patients in Europe, the U.S. has been much slower to make these products available, with only 15 biosimilars currently available to U.S. patients. In 2023, however, several already approved biosimilars for the biologic drug Humira are expected to enter the market. These biosimilars represent a major change in the biologics market because HumiraTM, a blockbuster drug approved for treatment for multiple clinical indications such as rheumatoid arthritis and psoriasis, consistently ranks as the drug with highest healthcare spending in the U.S.

Our findings from the NeupogenTM/ZarxioTM case suggest that savings from lower biosimilar drug acquisition costs are not directly translating to lower negotiated administered drug prices for ESI enrollees. If we see similar dynamics in other cases, the introduction of a biosimilar for Humira (and other biologics) may not substantially lower prices and spending among the ESI population, despite the lower biosimilar acquisition costs. This would represent a missed opportunity for savings among ESI enrollees, a population that pays disproportionately high prices. Unlike Medicare, where administered drugs are reimbursed prospectively based on ASP, ESI reimbursement of administered drugs is a product of negotiations between insurers and providers.

Smaller savings from biosimilar entry have real consequences for ESI enrollees and their families. When facing high costs, patients may have to make difficult choices between receiving treatment for cancer and other potentially devastating diseases and experiencing sometimes crushing medical debt, financing children’s education, and even providing necessary food and housing for their families—even when they have health insurance. Our findings suggest that it is important for policymakers to monitor the trend in ESI prices to gain a complete and robust picture of the effect of biosimilar entry on all insurers and patients.